On the Independence of Central Banks

How the mood of the times can influence decisions.

These days one has to be either deaf or very stupid to defend any “establishment” conventions on governing bodies. Well, I’m either deaf or stupid – or both.

The independence of a country’s monetary authority, an almost untouchable “first” principle for decades, is now being questioned routinely by various groups (politicians, the press, economists, even London taxi drivers). Maybe this new analytical thrust is just part of the pattern I hinted at in the preceding paragraph, where every established paradigm is being challenged in many democracies of the West. Or maybe this one is different inasmuch as its causes are less structural in nature and more spur of the moment.

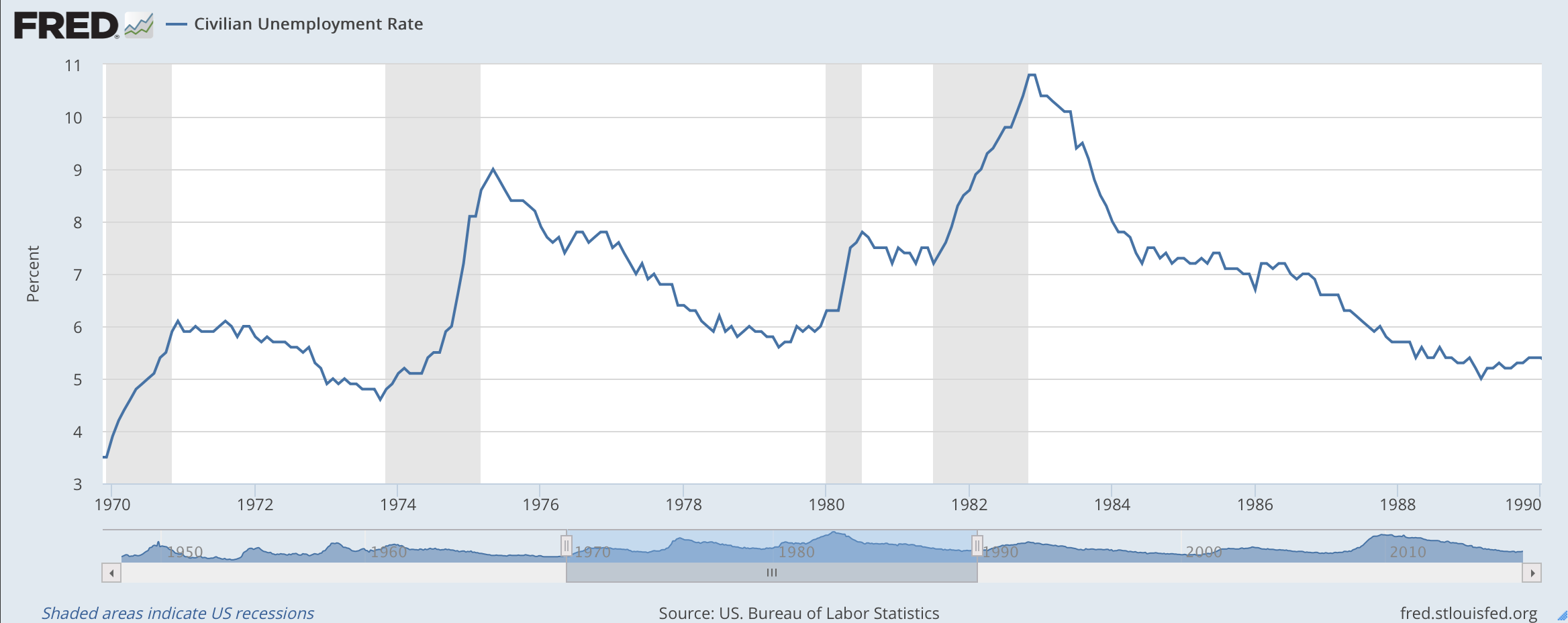

I can’t avoid smiling when I think of how in the late seventies and early eighties we all squirmed under the horrific squeeze imposed on us by Paul Volcker’s Fed. One graph will suffice: look at what happened to unemployment in the US during that period, shooting from 5.50%-5.75% to almost 11%:

Figure 1

It was tough but necessary action. Yet the Fed was ultimately supported by most and its policies led to a string of prosperous years. I may be mistaken, but I don’t recall much talk of reining in Fed powers or burning any FOMC member at the stake.

Now fast-forward to 2016. Despite an unemployment picture diametrically opposed to the one engendered by Volcker (see Figure 2; whether with the help or the hindrance of monetary policy is beyond the point), hardly any day passes by without some utterance regarding the idiocy of persisting with a policy of 0% rates and how all central bankers should be brought within the confines of the decision making of the government in charge. Why? Because savers and investors are being penalized no end and because growth is not strong enough.

Figure 2

For me (remember, deaf and stupid) bringing central banks under the operational control of governments is just the equivalent of tossing out the baby with the bathwater. Central bankers make mistakes; they are human like the rest of us. As you know, I agree with those who criticize current monetary stance. But these matters are not enough to justify changing the current set of checks and balances; in fact, there is a much more fundamental danger in taking this action.

Think of it this way: governments have always been in charge of fiscal policy and look where that has gotten us. The theoretical construct of Keynesian fiscal policy always required expansionary budgets (producing a deficit) in bad times and contractionary action (to balance the budget) in good. But from the levels of debt common today it seems like the second half of the deal was never implemented, and since they feel they’ve run out of alternatives, politicians are now asking to take control of the other branch of economic policy management, the one that can put the brakes on their unbridled enthusiasm. That sounds plain foolish to me.

-Photo Sources-

Cover: http://business.financialpost.com/investing/investing-pro/joe-chidley-myth-of-central-bank-independence-exposed-as-fed-stands-pat