Timing Is Everything

So is luck; now what?

“Timing is everything” is a close relative of “luck is everything”. While it may be true that “the harder I work the luckier I get,” it’s clear that if you are not given the chance you simply won’t get it done – whatever “it” may be. For example, the journalist who took this picture perhaps was working harder than the fellow aiming his zoom in the other direction; still he needed to be there and no amount of work could have accomplished that:

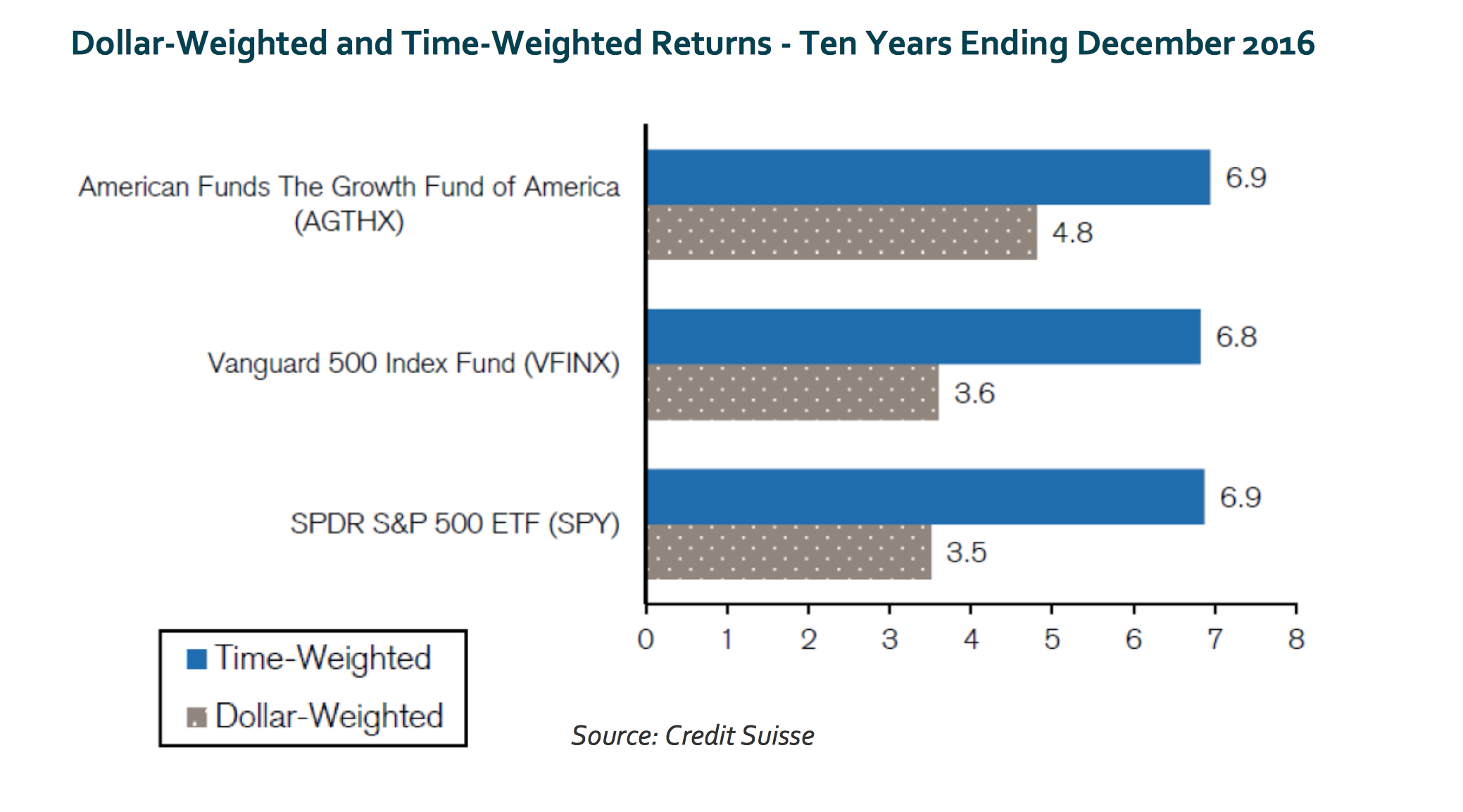

If timing is a bit like luck, it follows that it should be handled in an analogous manner. This concept eludes the world of investing where most participants spend a lot of time attempting to time the stock market. As a synopsis for other studies, here’s a picture of what getting in and out of the market means to investors’ pockets:

The differential between time-weighted returns (buy-and-hold) and dollar-weighted ones (in-and-out) is huge. Other things could perhaps partly explain the differential but most of it is attributed to failed market timing. Peter Lynch was right when he said: “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in the corrections themselves.”

So why do people do it? Maybe it helps if we ask the question in a slightly different manner: if the cost of attempting to time the market is so large, then what are long-term investors being compensated for and do they understand that? I think the answer is time: if you are a true long-term investor (as you should be when you are talking about equities), then you must realize you are getting paid to absorb the volatility of the market. That’s where the difference between roughly 7% and 4% comes from. If you can’t do that – because you want to make a major purchase in 6 months, or because you need to live by dipping unpredictably into your savings, or perhaps simply because you’re fidgety – then don’t invest. Keep the cash and continue serenely with your life.

Can the volatility be smoothed? There are a few things one can do. Despite this will sound a lot like “timing” (which it technically is), the trick is in finding the right indicators, the ones that represent demonstrably persistent phenomena which have shown up over more than a century of data. These indicators will typically involve time frames which are quite longer than the ones used for standard in-and-out activity. One of them is valuation (using parameters which eliminate the impact of the business cycle); another is momentum. Both methodologies require knowhow and patience, characteristics that are in short supply of course.

Basically, the question for most investors then is not “how do I get the timing right?” but “can I afford to do away with timing?” You’ll need a plan and the discipline in following it, which in turn means defining your investment horizon and, hence, your capacity to absorb volatility.

Simple.

-Further Readings-

My Current Reads – a list of the last 30 items (books, articles or blog posts) I found interesting: right column on HOME page, or under LIBRARY > MY CURRENT READS.

Research – economics and finance research papers: under LIBRARY > RESEARCH.

-Photo Sources-

Cover: http://www.lolwot.com/19-photographs-that-prove-that-timing-is-everything/5/

Rhino picture: http://www.theguardian.com/artanddesign/2016/mar/04/greg-armfield-mating-rhinos-nairobi-national-park-photograph?CMP=fb_gu