“Intuitive” Policy Is Often Wrong: Tax Code Edition

by Morgan Frank, Portfolio Manager, Manchester Explorer Fund

January proved to be a powerful up month for the broader markets which appeared to have a tailwind precisely obverse to the endless headwinds of November and December. Particularly among large and mid-caps, the moves were remarkably uniform and sudden. This would seem to bolster the hypothesis that much of the melt down in Q4 was driven by de-leveraging among large funds responding to higher volatility and the indexes going red on the year then driving and compounding aggressive tax loss selling. The market has now recovered substantively all of the December wipeout and returned to the 2600-2900 SPX trading band in which it spent most of 2018. Our guess is that this level will persist for the near future as a solid by not hot economy and labor market stalemate with trade policy driven losses and uncertainty about the political climate. With the legislature and executive branch now polyglot, we can expect even greater gridlock and rancor. Most of this will be a sideshow with “soundbites and fury signifying nothing”. Stalemate is generally good for the economy. Our fear is that the much vaunted “animal spirits” that drive investment and growth which are normally in fine humor during periods of governmental inactivity may be suppressed by the uncertainty created by the inevitable political posturing arising from the initial argy bargy of a crowded field of opposition hopefuls gearing up so seek the Democratic nomination for the presidency. Capital investment decisions at the corporate level are made with timeframes of 3-5 years in mind. That clearly crosses the election and means that its results, especially in light of the mid-term, may have significant impact. We have spoken in the past about the unusually bad set of economic ideas coming from the left recently. The run up to this election appears set to double and triple down on them.

The dueling banjos of reliably bad economic policy, Elizabeth Warren and Bernie Sanders, have been putting on a show that would have left Earl Scruggs slack jawed. Their competing plans to violate patent protection on pharmaceuticals in order to bring prices down would be so damaging to the development of such products as to set the US drug industry back 40 years. The general thrust of the 2 competing plans is to either break the patent and grant a right to make the drug to a generic manufacturer (Bernie) or to break the patent and have a government agency make the drug (Liz). This is a truly dangerous idea that invalidates law and business sense alike. Price is one of the most important and least understood signals in an economy. Distorting it tends to have severe repercussions from mortgage crises to housing shortages to famine to the destruction of whole industries. Mass market drugs cost billions to develop and test. This cost must be recouped by sales. In this, they are much like software. The first copy of Windows 10 costs $9 billion. The second costs 8 cents. But to base assumptions about sales price and “gouging” upon the cost to make the 1000th copy is to miss the game entirely. The initial investment is the hard part and if Microsoft were, for example, told that they can only mark-up Windows 100% from cost to produce and were forced to sell it at 16 cents a copy, sure, it’s cheap for a minute, but would another version EVER be developed? Drugs are no different. The only way to induce development is profits. This policy would be ruinous. Fortunately, it’s probably illegal/unconstitutional.

More threatening is the topic on which the chorus has so vociferously joined in that even the banjo players are struggling to keep up and avoid being drowned out: taxes. The currently resurgent socialist wing of the Democratic party has all manner of pet projects from single payor health care to “free” college for all and universal basic income that all need paying for. The classic answer from atop the soapbox when asked “and how does sir or madam propose to pay for this?” is “tax the rich.” This plays well with most of the demos. After all, who does not like being taken out to lunch on someone else’s dime, especially if you get to pick the wine? There is just one problem with this policy proposal: it will not and cannot work.

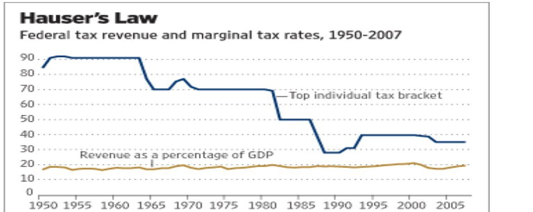

We have spoken in the past about Hauser’s law. For those who have not been long term readers, a quick primer: the Laffer curve states that the tax dollars collected at various tax rates is 0 at 0%, 0 at 100%, and has a peak somewhere in between. It never ceases to amaze us how this literally mathematically certain observation is so maligned as some sort of tax dodger policy, but what can one do? An interesting instantiation of this idea is Hauser’s law which shows us the shape of this curve in the US. It states, quite simply, that federal tax receipts in the US, measured as a % of GDP, are remarkably constant at 19% +/- 1%. Of extreme interest here, this figure appears to be completely independent of the top tax rate. If anything, receipts have risen slightly as tax rates have dropped.

This implies that the 70% (and higher) tax rates currently being discussed by many leading Democrats would not raise a cent of additional taxes. How can this be? Simple. Those facing such tax rates have intense incentive to structure their income to avoid such confiscatory levels of taxation. So they devote far more time, energy, and resources to tax avoidance. The arms race of IRS vs Jeff Bezos’s tax lawyers might as well be a tortoise chasing a cheetah. But the time, energy, and capital this tax avoidance costs takes assets away from investment in the productive. So you get less overall growth. This means that the 19% taken in 5 years from now is of a smaller pie than it could have been and represents fewer actual dollars. It’s a disastrous policy with no hope of success. If only such a thing had any real effect on the likelihood of such ideas being adopted as policy… (see also: trade wars)

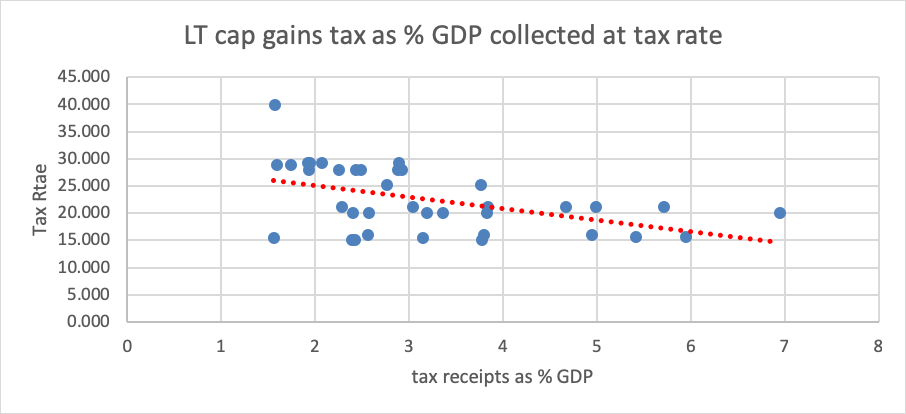

To greatly worsen this issue, the nature of compensation has changed greatly. If one examines the super-rich in the US today, the wealth is not a function of income but of equity. This would seem to shift the key issue to the capital gains tax. This, alas, is the tax that has the MOST effect on future growth rates as it directly increases the cost of capital and small moves matter an enormous amount. Consider a one-year investment. You demand an 8% rate of return to compensate you for that risk. So, if you will pay tax at 20%, you need the base investment to appreciate by 10%. This becomes the necessary cap rate to induce you to risk capital. But what if the tax rate is 40%? Now you need 13.3%, a 33% rise in expected return to induce you to leave the sidelines. Such a leap would eliminate a great many projects at the margin. This also got us to thinking: “is there a form of Hauser’s law that applies to capital gains taxes?” We were unable to find anyone who had done this work, so, because we are what can charitably be called “econ dorks” we did the analysis ourselves using a dataset running from 1954 to 2014. (if anyone has this data for earlier or later periods, please let us know, we’d love to see it.) The results were striking. In that period, the cap gains tax rate has varied from a low of 15% to a high of 39.875. We looked at a number of ways to express the results and this was the best that we have found. It is a scatterplot of annual data points plotted in rate/receipts space.

The relationship is quite compelling. The higher one raises the tax rate, the lower the tax receipts as a % of GDP. We even trend tested it to eliminate the possibility of spurious high results from people waiting to take gains until a cut occurred then taking them right after. That issue does not appear in the data. What does appear is that of the 7 times receipts exceeded 4%, 100% were at a tax rate under 22%. Every one of the top 10 was. Of the 7 below 2%, 6 had a tax rate above 22%. Even the averages are striking. The average cap gains tax receipts as a % of GDP in this period was 3.19%. For periods with a tax rate greater than 22% it was 2.35%. For periods below 22%, it was 3.77%. You get 60% more tax income as a % of GDP with sub 22% rates than with greater than 22% rates. For the econometrics geeks among you, the t-statistic on the tax rate (as the indep value) is -3.23 significant at the p=0.002 level (and nearly to 0.001) implying there is less than a 1 in 500 chance this is random. That represents a truly staggering differential even before one applies the difference in GDP growth rates. This pretty much drives the final nail into the coffin of these “soak the rich” policies. This is not a viable way to fund massive new spending programs. As with trade, we think it is important to use accurate lenses to view the actual effects of these increasingly populist and popular policies of which both sides of the American political spectrum seem so enamored. If nothing else, we hope we have provided you with amusing fodder with which to annoy people at cocktail parties.

Photo Cover – https://goldsilver.com/blog/stockman-it-beginsamericas-state-wreck-is-building-momentum/