Why Wouldn’t You Invest in Stocks

All politics is local. Together with real estate and food. Regional is perhaps a better word. Despite all the rationalizing capacity we attribute to humans, we usually revert to our surroundings. This may not be so bad; take food for example: where would we be without the uncountable variations offered us by regional cuisines? A miserable world indeed.

In constructing equity portfolios, regional biases are usually not recommended but they persist anyway. It’s called “home bias”: Americans will have far more US equities than they should; Europeans hug local stocks. You could argue convincingly that in today’s world of global companies it does not really matter where their domicile is; also, countries are becoming less important and sectors should be the focus.

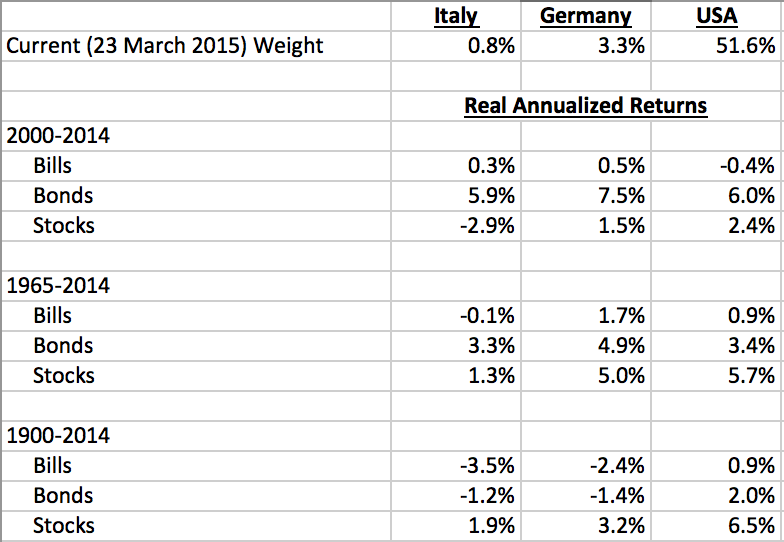

The above arguments though do not justify another form of “bias”: how investors in various locations embrace the idea of an equity-driven portfolio. The Financial Times had an excellent article last Saturday on the subject (Germans miss out on Dax bonanza as share ownership drops by third). I have been familiar with the issue for some time. As a simple observation, a 70/30 bond/stock portfolio in Italy is perceived as the equivalent of a 50/50 in the US. I pulled some figures from the CS Global Investment Returns Yearbook 2015 to see if history could justify these divergences; they are reported below.

Focusing on the first two periods listed – after all, “In the long run we are all dead” -, it is striking how similar the German and US experiences have been; yet per the FT article German investors find equities “untrustworthy” or “speculative” in nature. Italians (included for my personal regional issues) are perhaps excused for their mistrust of equities though of course no one limits them to the local market. Neither Germans nor Italians (or other Europeans) make any sense to me when you see how much they focus and truly speculate on currencies – among the most unpredictable and return-less “things” around. While 30% in equities is “balanced”, 10-25% currency bets are considered normal manager prerogative. Rationality is out the window.

I don’t have a good answer to these observable skews in investor behavior: home bias, asset-class bias, structural local savings and pension laws, investment advisory business constraints, genetic or ancestral proclivities; who knows? The last 115 years afforded the US the trophy for best large market (best overall is Australia), but American large-caps are accessible and well known all over the world; they are sometimes even listed in local exchanges. Entrepreneurial spirit, greedy or not, is culturally more acceptable in certain societies (but what to make of the currency betting craze?). It’s further possible the answer lies with how society perceives short-term volatility. This does not validate the long-term argument. But if you just can’t lift your neck above the water line then maybe you really never will invest in stocks.

Whatever it may be, from an investor’s point of view it may cost dearly.

Photo source: investorchamp.com, independent advisor.

1. Roberto, you forgot to mention Gold as one of the most unpredictable and return-less “things”. I’ve always wondered on what basis “specialists” issued buy/sell recommendations on such a popular “thing”

2. It’s inevitable that people have a bias for local stocks. Thanks to proximity you know more than a company’s financials (you could more likely be client or supplier, be the target of the company’s ads, know well someone who works there).

On gold you are absolutely right; it must be that I still have the flu, otherwise I wouldn’t have missed it.

On the second point, while I agree the factors you list could influence investors towards a local bias, it is also true that today you can access the whole world with one ETF – obtaining diversification and other returns without being forced to stock pick.

I think one reason for preferring local companies is given by the fact that one prefer to hold equities of companies you know. Especially if you are not a full time asset manager. But even then it is easier to tell the story convincingly.

For the German public I think a lot of people got hit by the T-com crash and since then it is even more unlikely that someone buys shares. Shares are either for experts (risky) or unethical is what I hear a lot in Germany.

Last but not least if you invest in companies around the world you should also make sure you hedge your currency risk. If this is to complicated it gets tricky. But imagine a solid investment in Japan – the FX trend might have taken away all your return. But now-a-days you can buy hedged ETFs. So this shouldn’t be a problem.

Those are all very good points Andreas.

Very nice post! And thanks for photo source credit!